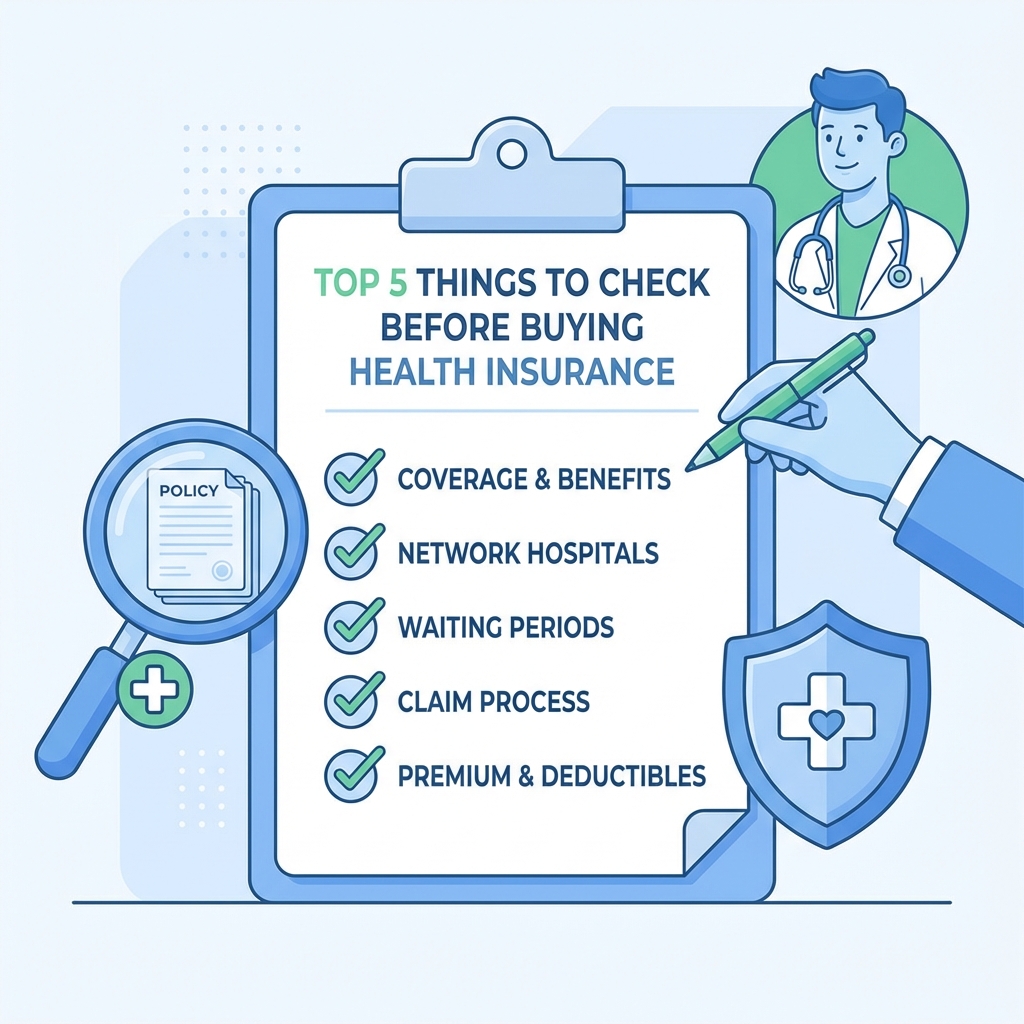

Top 5 Things to Check Before Buying Health Insurance

A practical checklist to ensure you're buying the right health insurance policy without costly coverage gaps

Why This Matters

Health insurance claims are often rejected due to coverage gaps, fine print clauses, and exclusions. By checking these 5 critical factors before buying, you can avoid surprises when you need coverage the most.

The 5 Essential Checks

Sum Insured (Coverage Amount)

Sum Insured is the maximum amount the insurance company will pay for your medical treatment. This is critical because insufficient coverage can leave you paying out of pocket during emergencies.

What's the Right Amount?

- Minimum ₹5 Lakh: Basic coverage for individuals

- ₹10-15 Lakh: Recommended for families (family of 4)

- ₹25+ Lakh: If you're above 45 or have health issues

Red Flag Example

A patient was hospitalized for 20 days with ₹3 Lakh in bills, but his policy had only ₹2 Lakh coverage. He paid ₹1 Lakh out of pocket. Don't let this happen to you!

Room Rent Cap & Proportion Deduction

Room Rent Cap is the maximum daily hospital room cost the insurer will reimburse. Exceeding this cap can trigger "proportionate deduction" where they reduce your entire claim reimbursement.

How Room Rent Impacts Your Claim

Example:

- • Total Hospital Bill: ₹5 Lakh

- • Room Rent Charged: ₹5,000/day (20 days = ₹1 Lakh)

- • Your Policy Room Cap: ₹2,000/day

- • Reimbursement Reduced to: ₹4 Lakh (20% deduction on entire bill)

- • You Pay Out of Pocket: ₹1 Lakh

What to Look For

- Room cap should be at least ₹3,000-5,000/day

- Better plans offer "Unlimited" room rent

- Check if room rent is calculated as % of sum insured or as absolute limit

Pre-Existing Disease (PED) Waiting Period

Pre-Existing Disease (PED) waiting period is how long you must wait before claims related to existing health conditions are covered. This is a major clause that can significantly impact your coverage.

Typical PED Waiting Periods

Critical Alert

If you have diabetes or hypertension, you MUST disclose it during application. Non-disclosure can lead to claim rejection even after the waiting period ends!

Co-pay & Deductibles

Co-pay is the amount you pay out of pocket for each claim, while deductibles are annual amounts you must pay before insurance kicks in. These reduce your reimbursement significantly.

Understanding Co-pay vs Deductible

Co-pay (Percentage-based):

If your policy has 10% co-pay and your bill is ₹1 Lakh, you pay ₹10,000 and insurer pays ₹90,000

Deductible (Amount-based):

If your policy has ₹5,000 deductible and your bill is ₹50,000, you pay ₹5,000 and insurer pays ₹45,000

Best Options

- Zero co-pay (full reimbursement)

- Or low deductible (₹1,000-5,000 max)

- Some plans waive co-pay for network hospitals

Exclusions & Inclusions

Exclusions are conditions and treatments NOT covered by the policy. Some are standard, but reading fine print can reveal unexpected exclusions that leave you unprotected.

Common Exclusions to Watch

- Cosmetic/aesthetic procedures

- Treatment abroad (unless specifically included)

- Claims from high-risk activities or sports

- Mental health treatments (check coverage)

- Some fertility/pregnancy-related treatments

Must-Have Inclusions

- Pre & post-hospitalization expenses

- Day-care procedures (surgery without overnight stay)

- Outpatient consultations (critical!)

- Ambulance charges reimbursement

- Network hospital access (wider network = better)

Ready to Buy the Right Health Insurance?

Use our policy comparison tool to evaluate plans side-by-side and avoid coverage gaps

Quick Checklist for Buying Health Insurance

Sum Insured: Minimum ₹5L for individual, ₹15L+ for families

Room Rent: Should be unlimited or at least ₹3,000-5,000/day

PED Waiting: Choose plans with shorter waiting periods if you have existing health issues

Co-pay/Deductible: Prefer zero co-pay or low deductibles

Exclusions: Read the policy wordings carefully for hidden exclusions