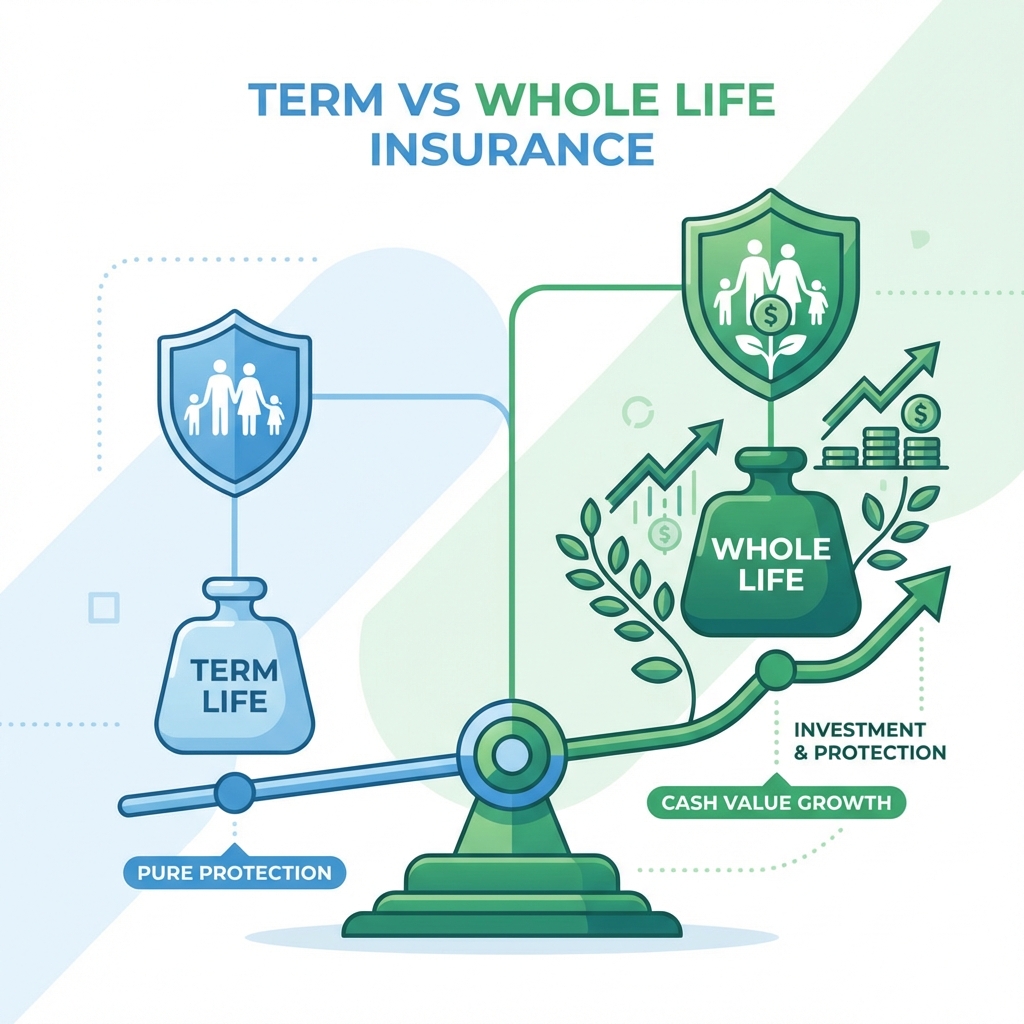

Term Insurance vs. Whole Life: Which is Right for You?

Understanding the key differences between term and whole life insurance policies to make the best choice for your family. We break down costs, benefits, and ideal scenarios.

What is Term Insurance?

Term insurance is the simplest form of life insurance. You pay a fixed premium for a specific term (usually 10-30 years), and if you pass away during that term, your beneficiaries receive the death benefit. If you outlive the term, the policy expires and you get nothing back.

Key Features of Term Insurance:

- • Pure protection - no investment component

- • Lowest premiums for maximum coverage

- • Fixed premiums throughout the term

- • Simple and transparent

- • Tax benefits under Section 80C

What is Whole Life Insurance?

Whole life insurance provides coverage for your entire lifetime, as long as you pay the premiums. It combines a death benefit with a cash value component that grows over time. You can borrow against this cash value or surrender the policy for its accumulated value.

Key Features of Whole Life Insurance:

- • Lifetime coverage

- • Cash value accumulation

- • Higher premiums than term insurance

- • Investment component

- • Policy loans available

Head-to-Head Comparison

| Feature | Term Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Period | Fixed term (10-30 years) | Lifetime |

| Premium Cost | Low (70-80% cheaper) | High |

| Cash Value | None | Yes, grows over time |

| Investment Returns | None (pure protection) | Low (4-6% typically) |

| Complexity | Simple | Complex |

Which One Should You Choose?

Choose Term Insurance If:

- • You want maximum coverage at minimum cost

- • You have dependents who rely on your income

- • You're comfortable investing separately for better returns

- • You need coverage only until retirement

- • You prefer simplicity and transparency

Choose Whole Life Insurance If:

- • You need lifelong coverage (estate planning)

- • You want forced savings discipline

- • You prefer an all-in-one solution

- • You don't want to manage separate investments

- • Estate tax planning is important for you

The Smart Money Approach

For most people, the best strategy is "Buy Term and Invest the Rest." Here's why:

Example Calculation:

Scenario: 30-year-old male, ₹1 crore coverage

- • Term Insurance Premium: ₹8,000 per year

- • Whole Life Premium: ₹35,000 per year

- • Savings: ₹27,000 per year

If you invest the ₹27,000 savings annually at 10% returns:

- • After 20 years: ₹15.4 lakhs

- • After 30 years: ₹44.4 lakhs

Final Recommendation

For 95% of Indian families, term insurance is the better choice. It provides the protection you need at a fraction of the cost, leaving you with more money to invest for your other financial goals.

Only consider whole life insurance if you have specific needs like estate planning or if you absolutely cannot discipline yourself to invest separately.

Need Help Deciding?

Our insurance experts can help you choose the right policy based on your specific needs, budget, and financial goals.